Cheap Chinese high-tech goods have flooded the global economy this year, raising alarms in Washington and Brussels as Western businesses complain about what they see as a new round of unfair competition.

Chinese leader Xi Jinping has dismissed the charges, saying “there is no so-called problem of Chinese overcapacity.” Instead, Chinese officials say the country’s electric vehicles, solar panels and other products are simply better and more competitive than Western versions.

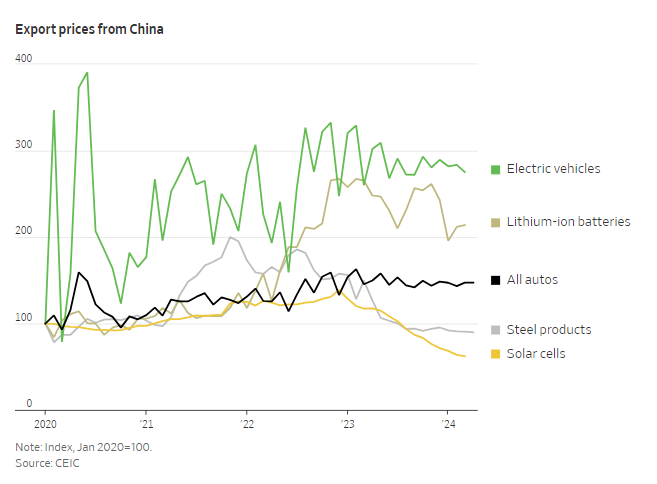

But a look at China’s industrial sector shows clear signs of overcapacity, especially in industries such as solar panels, automobiles and steel. In some sectors, the situation looks poised to get worse, as China keeps expanding capacity even as domestic demand stays weak.

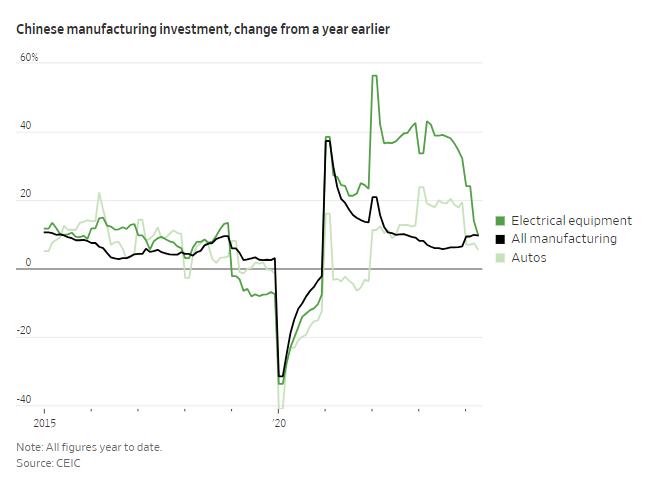

Chinese companies have invested more in manufacturing than usual, even though domestic demand and exports have often been weak. The trend has been especially stark for certain sectors that are favored by Beijing and often benefit from subsidies, such as EVs.

Auto-sector investment growth hit nearly 25% year-over-year in early 2023. The investment surge in solar panels, chips and batteries has been even more impressive.

As investment has surged, profit margins for Chinese producers have plummeted, especially for autos and steel.

Net profit margins for China’s manufacturing sector as a whole were under 4% in early 2024, well below average levels of around 6% in the late 2010s.

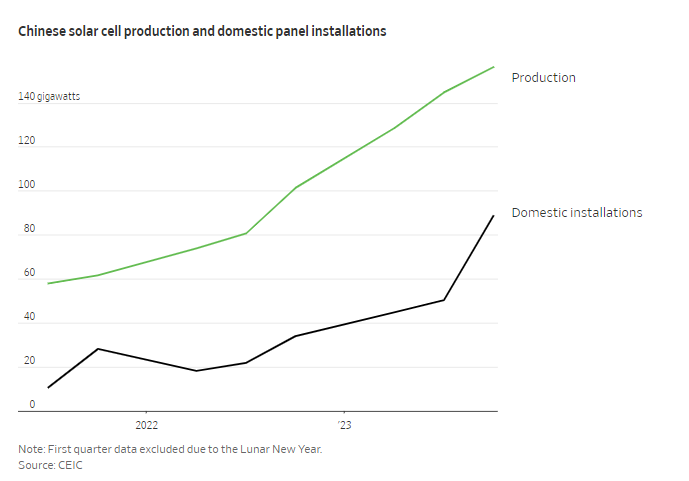

China’s excess capacity looks worst in solar-cell manufacturing, which, along with other clean energy applications, is one of the so-called “new productive forces” that Beijing has highlighted as central to its future growth strategy.

China in 2023 produced over 450 gigawatts of solar cells, according to official data. It installed less than 220 gigawatts at home—a massive figure but still less than half of what it produces.

The investment surge in China’s auto sector in 2022 and 2023 is now cooling. Investment, which was growing at nearly 20% year on year in 2023, has fallen to 5.7%, roughly in line with the historical average. Profit margins also appear to have stabilized, albeit at a lower level than in the past.

In other words, while overcapacity remains severe, it may no longer be rapidly worsening. An auto price war in China and slower EV adoption abroad seem to finally be curbing the investment mania at home.

Margins in electrical equipment, however, are trending down again—another warning sign for solar cells and other equipment like batteries.