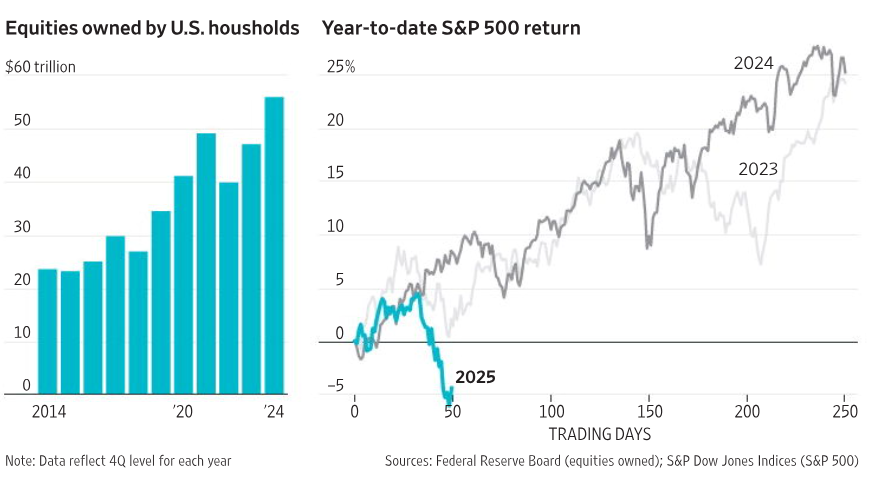

The U.S. equity market has been a cornerstone of wealth creation for American households over the past decade, as evidenced by the steady rise in equities owned by U.S. households from 2014 to 2024.

The Rise of U.S. Household Equity Ownership (2014–2024)

The U.S. stock market experienced a prolonged bull market for much of this period, driven by low interest rates, technological innovation, and strong corporate earnings. Companies in sectors like technology, healthcare, and consumer discretionary—think Apple, Amazon, and Tesla—saw their valuations soar, contributing to the overall increase in equity values.

The democratization of investing played a significant role. The rise of commission-free trading platforms like Robinhood and the proliferation of retirement accounts (e.g., 401(k)s and IRAs) made it easier for the average American to participate in the stock market. By 2024, a larger share of U.S. households had exposure to equities, either directly through stock ownership or indirectly through mutual funds and ETFs.

Analyzing the S&P 500 Performance (2023–2025)

2023: The S&P 500 in 2023 shows a relatively stable performance, with year-to-date returns hovering around 5% to 10% for much of the year. This suggests a year of moderate growth, likely driven by a recovering economy following the challenges of the early 2020s, including the COVID-19 pandemic and subsequent inflationary pressures. The Federal Reserve’s efforts to manage inflation through interest rate hikes may have tempered market exuberance, but the overall upward trend indicates resilience in corporate earnings and investor confidence.

2024: The S&P 500’s performance in 2024 is striking, with year-to-date returns reaching nearly 25% by the end of the period shown. This suggests a robust bull market, possibly fueled by a combination of factors such as declining inflation, a more accommodative Federal Reserve policy (potentially lowering interest rates), and strong economic growth. Sectors like technology and artificial intelligence likely played a significant role, as companies leveraging AI innovations saw their stock prices soar. The steep upward trajectory in 2024 reflects a period of optimism and risk-on behavior among investors.

2025: In stark contrast, 2025 shows a sharp decline, with year-to-date returns dropping to around -5% within the first 50 trading days. This early-year sell-off could be attributed to several potential factors: a sudden economic shock, such as a geopolitical event, a resurgence of inflation, or a policy misstep by the Federal Reserve. Alternatively, it might reflect a market correction following the exuberance of 2024, as valuations in certain sectors (e.g., technology) may have become overstretched. The volatility in 2025 underscores the cyclical nature of markets and the challenges of sustaining prolonged periods of growth.

Economic Factors Driving Equity Ownership and Market Performance

The trends in these charts cannot be understood in isolation—they are deeply tied to broader economic conditions. From 2014 to 2024, the U.S. economy experienced a mix of challenges and opportunities that shaped equity ownership and market performance.

Monetary Policy: The Federal Reserve’s policies have been a major driver of equity markets. From 2014 to 2019, low interest rates and quantitative easing provided a tailwind for stocks, as investors sought higher returns in equities rather than bonds. The early 2020s saw a shift, with the Fed raising rates to combat inflation, which led to market volatility. By 2024, a potential easing of rates may have contributed to the S&P 500’s strong performance, while the decline in 2025 could reflect a reversal of this trend or unexpected tightening.

Technological Innovation: The growth in equity values has been heavily influenced by the tech sector. Companies like Microsoft, Nvidia, and Alphabet have driven much of the S&P 500’s gains, particularly in 2023 and 2024, as they capitalized on trends like cloud computing, AI, and digital transformation. However, the sharp decline in 2025 might indicate a reassessment of these valuations, as investors question the sustainability of growth in these sectors.

Household Behavior: The rise in equity ownership also reflects changing attitudes toward investing. The “meme stock” phenomenon of 2021 (e.g., GameStop and AMC) and the popularity of retail investing platforms encouraged more Americans to enter the market. Additionally, the shift toward passive investing—through index funds and ETFs—has made it easier for households to gain exposure to the S&P 500, contributing to the growth in equity ownership.

العربية

العربية 简体中文

简体中文 English

English