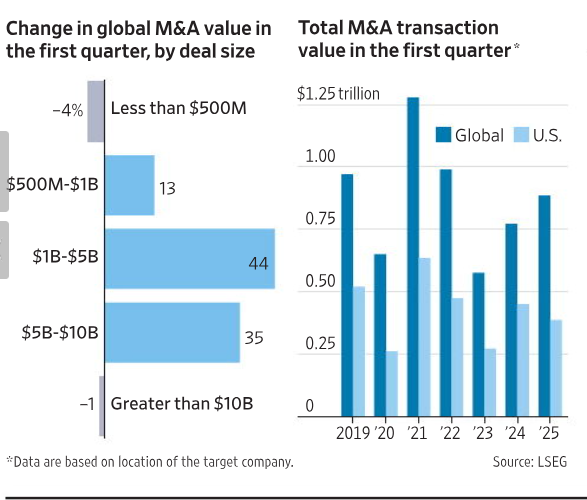

Mergers and Acquisitions (M&A) have long been a barometer of economic health, reflecting corporate confidence, market dynamics, and global financial trends. The first quarter of each year often sets the tone for M&A activity, providing insights into how businesses are positioning themselves for growth or consolidation. This article examines the change in global M&A value in the first quarter by deal size and the total M&A transaction value from 2019 to 2025, with a particular focus on both global and U.S. markets.

Drivers Behind the Trends

Several factors have influenced the observed M&A trends:

- Economic Conditions: The spike in 2021 was fueled by low interest rates and government stimulus, which provided companies with the capital to pursue acquisitions. The subsequent decline in 2022–2023 reflects the impact of rising interest rates and inflation, which increased the cost of borrowing and dampened deal activity.

- Sector-Specific Dynamics: The growth in $1B–$5B and $5B–$10B deals may be driven by sectors like technology, healthcare, and renewable energy, where companies are seeking to acquire innovative firms or consolidate market share. For example, tech companies may be acquiring AI startups, while healthcare firms pursue mergers to address aging populations.

- Regulatory Environment: The lack of growth in mega-deals (greater than $10B) could be attributed to increased regulatory scrutiny, particularly in the U.S. and Europe, where antitrust concerns have delayed or blocked major transactions.

- Geopolitical Factors: Tensions such as the Russia-Ukraine conflict and U.S.-China trade disputes have created uncertainty, impacting cross-border M&A activity. However, the projected growth in 2025 suggests that companies are adapting to these challenges.

Implications for the Global Economy

The trends in M&A activity have broader implications for the global economy:

- Corporate Strategy: The focus on mid-to-large deals indicates that companies are prioritizing strategic growth over speculative or high-risk mega-deals. This could lead to more sustainable growth in industries like technology and healthcare.

- Economic Recovery: The projected increase in M&A value for 2025 suggests optimism about economic recovery, as companies are willing to invest in long-term growth. However, the decline in smaller deals raises concerns about the health of startups and mid-sized firms, which are often key drivers of innovation.

- U.S. Market Dominance: The U.S. consistently accounts for a significant portion of global M&A value, reflecting its role as a hub for corporate activity. The chart shows that U.S. M&A value closely tracks global trends, underscoring the interconnectedness of the two markets.

- Investor Confidence: Rising M&A activity, particularly in 2024 and 2025, signals growing investor confidence, which could have positive spillover effects on stock markets and economic growth.

Our Opinion

The M&A landscape in the first quarter from 2019 to 2025 reflects a dynamic interplay of economic, regulatory, and geopolitical factors. While smaller deals have struggled, mid-to-large deals have driven growth, signaling a strategic focus on transformative acquisitions. The projected $1.25 trillion in global M&A value for 2025 suggests a robust outlook, with the U.S. continuing to play a leading role.

Looking ahead, companies will need to navigate challenges such as regulatory scrutiny, rising interest rates, and geopolitical uncertainty. However, the resilience of M&A activity in the face of these headwinds bodes well for the global economy. The chart provided offers a clear visual summary of these trends, highlighting the opportunities and challenges that lie ahead for corporate deal making.

العربية

العربية 简体中文

简体中文 English

English