In recent years, the U.S. corporate landscape has faced significant turbulence, with bankruptcy filings emerging as a critical indicator of economic health. This article delves into the trends, underlying causes, and implications of these figures, offering a comprehensive look at how businesses have navigated an era marked by global pandemics, inflation, and shifting market dynamics. As of March 18, 2025, the data provides a snapshot of a challenging period for American enterprises, raising questions about resilience, policy responses, and future outlooks.

Overview of the Data

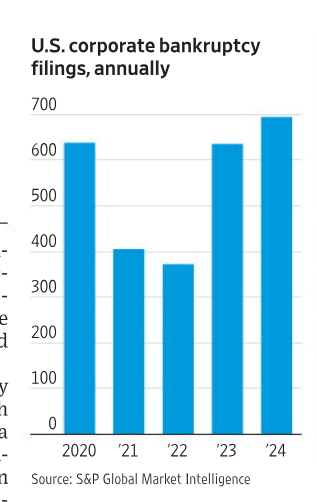

The chart reveals a fluctuating yet upward trend in bankruptcy filings over the five-year period. In 2020, the U.S. saw approximately 600 filings, a number that dipped to around 400 in 2021 before climbing back to 600 in 2022. The trend continued upward, reaching approximately 650 in 2023, and surged to over 700 in 2024. This rollercoaster pattern suggests a complex interplay of recovery and relapse, with the latest figures indicating a potential crisis point. The data underscores the volatility businesses have endured, particularly in the post-pandemic era, and sets the stage for a deeper exploration of contributing factors.

The Pandemic’s Initial Impact (2020)

The year 2020 marked the onset of the COVID-19 pandemic, which triggered unprecedented economic disruption. With lockdowns and supply chain breakdowns, many businesses—especially in hospitality, retail, and travel—struggled to survive. The 600 bankruptcy filings in 2020 reflect this initial shock, as companies faced cash flow shortages and declining revenues. Government stimulus packages, such as the Paycheck Protection Program (PPP), provided temporary relief, but for many, it was insufficient to offset the prolonged uncertainty.

The 2021 Dip and Recovery Hopes

The decline to 400 filings in 2021 offered a glimmer of hope, coinciding with vaccine rollouts and the gradual reopening of economies. Businesses that adapted—shifting to e-commerce or streamlining operations—managed to weather the storm. However, this dip may also reflect a lag effect, as some companies delayed filings in anticipation of further aid or recovery. The lower number suggests a temporary stabilization, but the foundation for future challenges was already being laid.

The 2022 Resurgence

By 2022, bankruptcy filings rebounded to 600, signaling that the recovery was uneven. Rising inflation, supply chain bottlenecks, and interest rate hikes began to erode the gains made in 2021. Small and medium-sized enterprises (SMEs), particularly those with high debt loads, found it increasingly difficult to service loans. This resurgence highlighted the fragility of the economic recovery and the limitations of monetary support in addressing structural issues.

The 2023 and 2024 Surge

The sharp increase to 650 filings in 2023 and over 700 in 2024 paints a concerning picture. Escalating costs of goods, labor shortages, and a tightening credit market have pushed more companies over the edge. High-profile bankruptcies in sectors like technology and manufacturing have amplified the trend, suggesting that even well-established firms are not immune. The 2024 peak, the highest in the five-year span, raises alarms about a potential wave of defaults that could ripple through the economy.

Implications and Economic Context

The rising bankruptcy rates have far-reaching implications. Job losses, reduced consumer confidence, and strained supply chains are immediate concerns. For creditors and investors, the trend signals higher risk, potentially leading to tighter lending standards. Policymakers face the challenge of balancing inflation control with support for struggling businesses. As of March 2025, the data suggests that without targeted interventions—such as debt restructuring programs or tax relief—the situation could worsen.

Looking Ahead

Looking forward, the trajectory of corporate bankruptcies will depend on several factors: global economic stability, interest rate policies, and the ability of businesses to innovate and adapt. While some industries may consolidate or recover, others may face extinction. The chart serves as a stark reminder of the need for proactive measures to support corporate resilience. As we move through 2025, monitoring these trends will be crucial for understanding the broader economic landscape.

العربية

العربية 简体中文

简体中文 English

English