Gold has long been considered a safe-haven asset, often sought after during times of economic uncertainty, geopolitical tension, or inflationary pressure. Meanwhile, stock indices like the S&P 500 are barometers of corporate health and economic growth expectations. The stark contrast between the surge in gold ETF investments and the uneven performance of global stock markets in early 2025 raises critical questions: Are investors bracing for a downturn? Is the U.S. economy decoupling from Europe? And what does this mean for portfolio strategies moving forward?

First, inflationary pressures may be at play. While inflation in the U.S. and Europe had moderated somewhat by late 2024, unexpected supply chain disruptions—potentially tied to geopolitical tensions or energy market volatility—may have reignited fears of rising prices. Gold, often dubbed “the inflation hedge,” tends to attract capital when investors anticipate a decline in the purchasing power of fiat currencies.

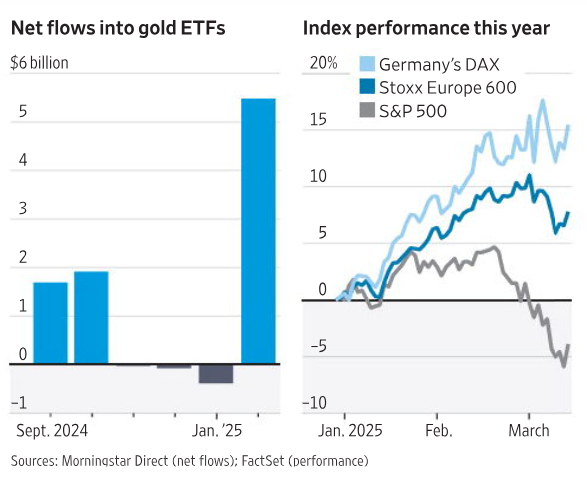

Second, geopolitical uncertainty could be a key driver. Early 2025 may have seen an escalation in global tensions—perhaps in regions like Eastern Europe, the Middle East, or the South China Sea—prompting investors to seek the safety of gold. Historically, events like the Russia-Ukraine conflict in 2022 or U.S.-China trade tensions in 2019 have driven similar spikes in gold demand. Finally, monetary policy dynamics might be contributing. If central banks, such as the Federal Reserve or the European Central Bank, signaled a pause or reversal in rate cuts in early 2025, investors might have turned to gold as a non-yielding asset that performs well in low or negative real interest rate environments. The $6 billion inflow in January 2025 suggests a significant shift in investor sentiment, one that warrants a closer look at the broader market context.

Stock Market Performance: A Tale of Two Continents

The right side of the chart illustrates the year-to-date performance of three major stock indices in 2025: Germany’s DAX, the Stoxx Europe 600, and the S&P 500. The contrast is striking. While the S&P 500 has gained approximately 15% by March 2025, the DAX and Stoxx Europe 600 have declined by around 5% and 7%, respectively.

The S&P 500’s strong performance aligns with historical trends of U.S. market resilience, often driven by the dominance of technology and consumer discretionary sectors. Companies like Apple, Microsoft, and Nvidia—key components of the S&P 500—may have continued to benefit from innovation in artificial intelligence, cloud computing, and consumer spending, even in the face of global uncertainty. Additionally, the U.S. economy may have shown relative strength in early 2025, with robust employment data, steady GDP growth, and a consumer base that remains willing to spend despite inflationary pressures.

In contrast, the declines in the DAX and Stoxx Europe 600 reflect a more challenging environment in Europe. Germany, as the economic powerhouse of the Eurozone, is particularly sensitive to energy prices and global trade dynamics. If energy costs spiked in early 2025—perhaps due to renewed tensions in the Middle East or disruptions in Russian gas supplies—German manufacturers, heavily reliant on energy-intensive production, would face significant headwinds. The DAX, which includes industrial giants like Volkswagen and Siemens, would naturally suffer.

The Gold-Stock Divergence: What It Means

The simultaneous surge in gold ETF inflows and the divergence in stock market performance is a classic signal of investor uncertainty. When gold prices rise while equities falter, it often indicates a flight to safety—a scenario where investors are more concerned with preserving capital than chasing growth.

This divergence is particularly pronounced between the U.S. and Europe. The S&P 500’s gains suggest that investors still have confidence in the U.S. economy, perhaps viewing it as a relative safe haven within the equity space. However, the massive inflows into gold ETFs suggest that this confidence is not absolute. Some investors may be hedging their equity exposure with gold, preparing for potential downside risks such as a U.S. recession, a tech sector correction, or a broader global slowdown.

In Europe, the picture is more uniformly bearish. The declines in the DAX and Stoxx Europe 600, combined with the gold surge, suggest that investors are deeply concerned about the region’s economic outlook. This could be a self-reinforcing cycle: as European stocks fall, investors move capital into gold, which further depresses equity valuations by reducing available investment capital.

From a portfolio management perspective, this divergence highlights the importance of diversification. Investors who were heavily weighted in European equities in early 2025 likely experienced significant losses, while those with exposure to gold or U.S. stocks may have mitigated some of the damage. The data underscores the value of gold as a non-correlated asset, capable of providing stability during periods of equity market volatility.

Broader Economic Implications

The trends depicted in the chart have far-reaching implications for the global economy. First, the surge in gold ETF inflows may signal broader inflationary fears. If investors are piling into gold because they expect prices to rise, this could pressure central banks to tighten monetary policy further, potentially slowing economic growth. In the U.S., where the S&P 500 is performing well, the Federal Reserve might face a delicate balancing act: maintaining growth while addressing inflation without triggering a market correction.

In Europe, the situation is more dire. The declines in the DAX and Stoxx Europe 600 suggest that the region may be on the brink of a recession—or already in one. If economic activity continues to contract, European policymakers may need to pivot toward stimulus measures, such as increased government spending or looser monetary policy. However, with inflation still a concern, their options may be limited, leading to a prolonged period of stagflation (high inflation combined with low growth).

Geopolitically, the gold surge could reflect heightened global risks. If tensions in key regions escalate, the resulting disruptions—whether in energy markets, trade routes, or financial systems—could exacerbate the economic challenges already facing Europe and potentially spill over into the U.S. The S&P 500’s gains may not be sustainable if global conditions deteriorate significantly.

Investor Strategies in a Volatile Environment

For investors, the data presents both challenges and opportunities. Those with a long-term horizon may view the declines in European stocks as a buying opportunity, particularly if they believe the region’s economic woes are temporary. Value investors might find attractive valuations in the DAX or Stoxx Europe 600, especially in sectors like industrials or financials that have been hit hard.

However, the surge in gold ETF inflows suggests that caution is warranted. Investors may want to maintain or increase their exposure to safe-haven assets like gold, particularly if they anticipate further volatility. Gold’s role as a portfolio diversifier is especially valuable in times like these, where traditional correlations between asset classes may break down.

In the U.S., the S&P 500’s strong performance may tempt investors to overweight equities, but the gold surge serves as a reminder to hedge against potential risks. A balanced approach—combining exposure to U.S. growth stocks with defensive assets like gold or Treasury bonds—could help investors navigate the uncertainty.

Finally, currency dynamics should not be overlooked. If the U.S. dollar strengthens due to its relative economic stability, gold prices (which are typically denominated in dollars) may face downward pressure. Conversely, a weaker euro could make European stocks more attractive to foreign investors, provided the region’s economic outlook improves.

Our Opinion

The first quarter of 2025 has revealed a financial landscape marked by uncertainty and divergence. The $6 billion inflow into gold ETFs in January signals a flight to safety, driven by inflationary fears, geopolitical risks, or monetary policy concerns. Meanwhile, the S&P 500’s 15% gain contrasts sharply with the 5-7% declines in the DAX and Stoxx Europe 600, highlighting a growing economic divide between the U.S. and Europe.

Looking ahead, investors will need to monitor several key factors: inflation trends, central bank policies, geopolitical developments, and corporate earnings. If inflationary pressures ease and Europe’s economic outlook improves, the divergence between gold and stocks may narrow, with equities potentially regaining favor. However, if global risks intensify, gold could continue its ascent, and European markets may face further challenges.

For now, the data serves as a reminder of the importance of adaptability in investing. By understanding the drivers behind these trends and maintaining a diversified portfolio, investors can position themselves to weather the volatility and capitalize on opportunities as they arise. The gold rush of early 2025 may be a harbinger of tougher times ahead—but it also underscores the enduring appeal of safe-haven assets in an uncertain world.

العربية

العربية 简体中文

简体中文 English

English