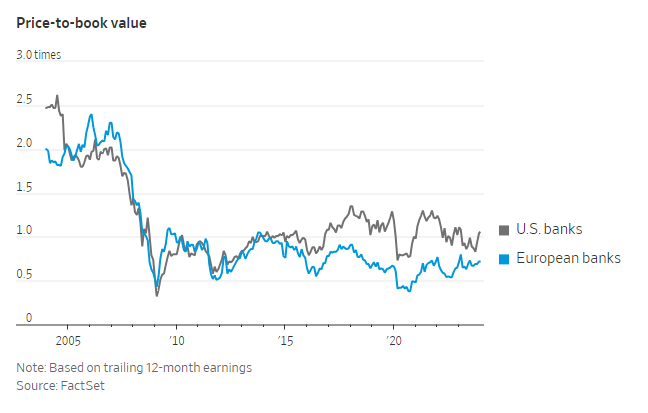

European lenders’ return on equity is now around 8%, compared with 12% across the Atlantic and 10% in Asia, in part as a result of stricter regulations following the 2008 banking crisis. Most European banks trade below book value on the stock market, having returned a negative 14% to investors since the April 2009 trough. Large American banks trade above book value and have gained 113%. In services particularly exposed to international competition, American banks dominate in Europe too: In 2023, they took the top five positions for mergers and acquisitions deals, Dealogic data shows, with France’s BNP Paribas coming in sixth, and the top six spots for issuing equity.

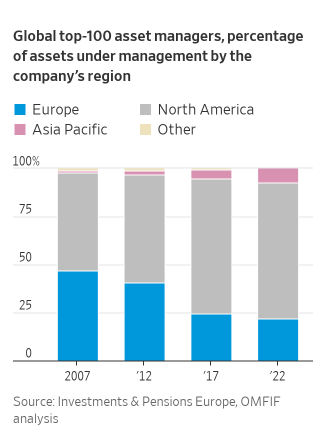

And this isn’t just about banks. In 2007, top European and U.S. asset managers roughly split the global market between them. By 2022, European fund managers had just 22% of total assets under supervision, with only France’s Amundi playing in the big leagues. This reflects their failure to jump on the train of low-fee passive investment as effectively as U.S. giants such as Vanguard and BlackRock. Ironically, the latter’s dominance in exchange-traded funds resulted from its acquisition of iShares from Britain’s Barclays in 2009.

The stock-market discount at which European lenders trade compared with American ones has shrunk over the past three years. But it is hard to see the tables fundamentally turning. In the digital era, economies of scale are even more powerful. The European Union comprises many countries with different languages, whose firms and investors have local financial relationships and strong home biases. The obstacles to eliminating fragmentation are huge.