Even Europeans are starting to wonder why they bother to invest in their own region.

The economy is stuttering while the U.S. booms. It’s an also-ran in a world dividing into blocs led by the U.S. and China. And its biggest companies wouldn’t even make the top 10 in the S&P 500. The “Magnificent Seven” big U.S. stocks are, as of two weeks ago, collectively worth more than all western European listed stocks together.

The European economy may not be as bad as it seems. And European stocks are cheap, so as bad as it is, much is already priced in. There’s one pushback: Since the end of 2021, the region’s stocks have actually been pretty good.

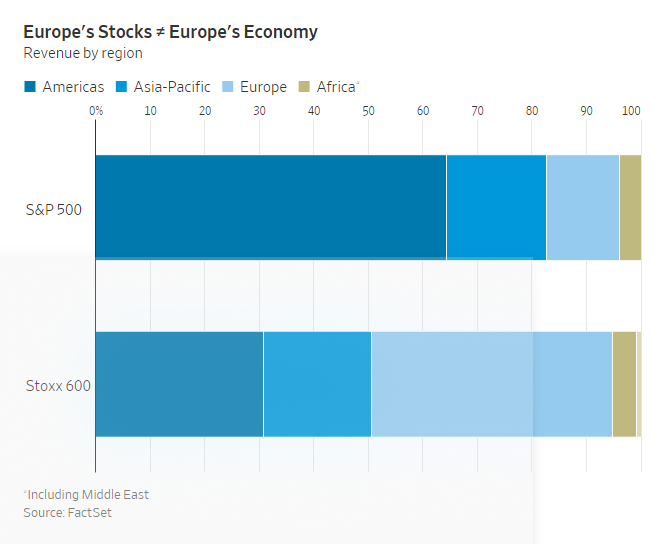

First, European stocks aren’t a very good way to bet on Europe. The market is dominated by multinationals: Successful ones include LVMH, the world’s biggest luxury-goods maker, and Denmark’s Novo Nordisk, maker of the diet drug Wegovy, as well as a bunch of much-less-successful ones, such as Volkswagen, whose shares are at the same level as in the summer of 2007. Firms in Europe’s Stoxx 600 benchmark make less than half their sales in Europe, according to FactSet data, and the U.S. is their single biggest market, at 23% of revenue. That compares with S&P 500 companies getting 59% of their revenue in the U.S. Britain is even more global, with companies in London’s FTSE 100 making more sales in the U.S. than in the U.K.

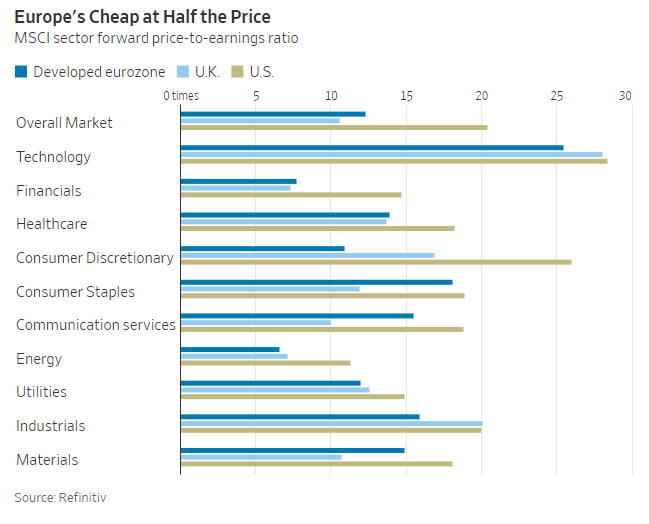

European stocks are cheap compared with the U.S., especially U.K. stocks. Even adjusting for the fact the U.S. indexes put more weight on big, expensive technology companies and Europe on cheap banks, Europe is still much cheaper.

Every European sector in the MSCI indexes trades at a lower price-to-earning ratio than those in New York. Compare the U.K., U.S., developed eurozone and Japan, and the U.K. is cheapest in five out of 10 sectors (I excluded real estate, where P/E isn’t an appropriate measure), the eurozone in two, and Japan in three. The U.S. is most expensive in five, Japan in three (communications, thanks to SoftBank, healthcare and consumer staples) and the U.K. in two (technology, ironically enough, where only two big London-listed firms survive, and industrials).

Focusing on the fact that European stocks don’t rely on the European economy is Mortier’s favorite way to buy the region, buying globally competitive companies that just happen to be European.

The problem is that everyone is doing this: Novo Nordisk, LVMH, the Dutch chip maker ASML and the airplane manufacturer Airbus, among others, are obvious leaders that can’t be ignored by any global investor.

Many Europeans have been giving up on their domestically focused companies, while foreign interest is nonexistent. That has made firms outside the superstar list very cheap. For investors who like to rummage for bargains, Europe, and the U.K. in particular, is the place to look.

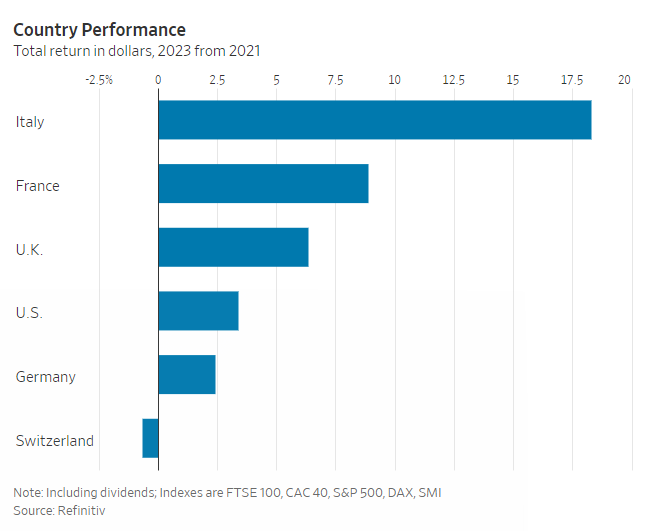

In 2022 and 2023 combined, Italy had the best-performing stock market in the Group of Seven leading advanced economies, in dollar terms, followed by France and the U.K., thanks to outperformance by banks. Switzerland, where Credit Suisse imploded, lagged behind. True, the U.S. ended 2021 at an all-time high with many sectors having extremely high valuations, while Europe was cheap. But, umm, look at the market now.